Confused by Your Credit Report? Here’s How to Decode It Easily

- Digital Marketing

- 3 days ago

- 3 min read

Ever looked at your credit report and felt completely lost? You’re not alone.

Finances are essential to life, and mastering them is key to building long-term financial stability. Yet, when it comes to reading a document, it still feels confusing. Therefore, it is necessary for you to learn that a credit report is for better understanding and better financial growth.

In this blog, we will see what important information about you and your finances is included in your credit report and develop an understanding of it.

What is a Credit Report?

Your credit report is a report card of your creditworthiness. It shows how reliable you are with the lender’s money. It includes information about your financial behaviour, such as how regular you are with repayments and how much of your total credit you are currently using. Your comprehensive Credit Report includes details like:

Your Repayment History

Credit Usage

Loan & Credit Card Details

Here’s how to Understand Your Credit Report.

Personal Information

This section shows your basic information, as mentioned below.

Your Full Name

Your Date of Birth

Your PAN number

Contact Information

Your Address

Your Employment Details

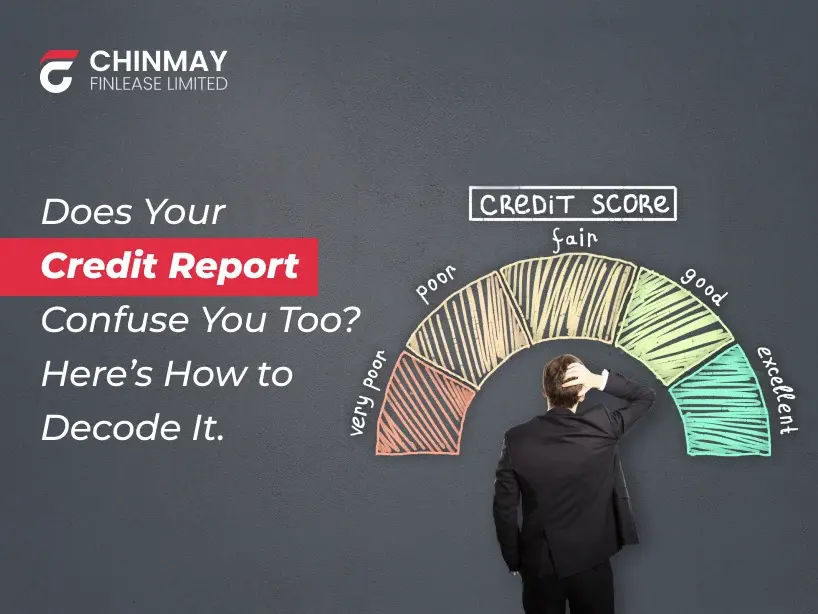

Credit Score

Your credit score is the first thing your lender checks before approving your loan application.

Credit Score ranges from 300 to 900.

Generally, a score above 750+ is considered good.

Here is a basic idea of the range where your credit score belongs:

800 to 900: Excellent

740 to 799: Very Good

670 to 739: Good

580 to 669: Fair

300 to 579: Poor

Account Information

This is one of the most important parts of your personal credit report, which includes:

Type of Account: The type of account shows the specific types of credit you have, such as credit cards, personal loans or mortgages.

Account Status: Indicates whether your accounts are closed or active.

Payment History: Your credit report shows the repayments you are making towards your existing debts.

Credit Limit (Credit amount): It shows your total available credit and how much of it you are currently using.

Current Balance: the amount of outstanding debt you still owe.

Account Open date: The date you opened the account.

Last Activity Date: The latest activity you performed on your credits.

Payment history

Your credit report shows your payment history, such as when you had tax issues, faced any legal objections in your finances or went bankrupt. These are the official records of your financial activity and history. These records impact your credit score and reflects into your report for the long term.

Credit Inquiries

When you apply for a personal loan, mortgage loan or a new credit card, your lender checks your credit score. This part of your credit report shows who has checked your credit report in past.

There are two types of credit inquiries:

Soft Inquiry: When you check your credit report or a lender who offers pre-approved loans, these two are types of soft inquiries. It does not affect your credit score.

Hard Inquiry: When you apply for a loan or credit card, a lender checks your credit; this is called a hard inquiry. It does affect your credit score.

When you apply for too many loans or credit cards in a short period of time, it affects your credit badly.

What information is not a part of your Credit Report?

Your Credit Score from Other Bureaus: Your credit report does not show the credit score derived by other credit bureaus.

Your Income: Income information is never included in your credit report. Despite this, your lender may request income information from you.

Your Bank Accounts: It does not include the number of bank accounts you have, such as salary or savings accounts.

Your Bank Balance: It does not show the balances of your various bank accounts.

Your Medical Bills: Medical bills paid by you are not a part of your credit report.

Your Crime Records: Your credit report is only an analysis that showcases your financial realities. It contains no other records, like crime records.

Where Can You Get Your Credit Report

Here are some official websites that offer genuine credit reports at your fingertips:

1. CIBIL

2. Experian India

3. Equifax India

4. CRIF High Mark

Conclusion

A credit report is not supposed to make you directionless. Rather, when you learn how to read your credit report, you can use it to take your financial health to another level. Whether you are applying for a personal loan through a bank or a trusted personal loan app, understanding your credit profile is a strong advantage. Also, educate yourself on the facts and myths about credit to better understand your report.

Always remember that your credit report matters more than you think, and at Chinmay, we believe that informed borrowers like you always make better financial decisions. So, stay ahead by regularly monitoring your credit and making smarter borrowing choices through the right loan app.

Comments